.svg)

Alpha Theory 2023 Year in Review

Alpha Theory data shows optimal position sizing outperforms actual sizing with a 92% win rate over 12 years. Learn how price targets, conviction, and systematizing your process can help you join the 10% who beat benchmarks.

For the twelve years of Alpha Theory’s dataset (2012-2023), a portfolio using Alpha Theory’s optimal position sizing outperformed clients’ actual sizing by an average of 4.3%. Optimal position sizing has demonstrated a 92% win rate, having outperformed eleven of the past twelve years. In 2023, optimal continued to outperform the average client, with the average client up +13.1% versus +17.8% for the average optimal portfolio.

Because Alpha Theory clients operate with ~125% of leverage vs. the industry median of ~150%, per a 10-year study from Morgan Stanleyi, analyses are based on Return on Invested Capital (ROIC).

The goal of publishing our data is to convince active fundamental managers that there is a better way to size positions. Even our own clients leave returns on the table. Over the past twelve years, the compound return is twice that of their actual performance, at 268% vs. 130%, and over 2.5x that of the average hedge fund, 268%ii vs. 94%. (Sidenote: four percent additional return for twelve years doubles the returns. Isn’t compounding amazing?)

HOW OFTEN DOES IT WORK?

On average, returns from optimal position sizing have topped returns from actual position sizing for 11 of 12 years. But it doesn’t win for every client and every position. If we randomly select a position, optimal sizing wins 55% of the time. If we randomly select a client, optimal sizing is better 69% of the time. What we see in the results is the benefit of consistently applying process. The more time spent applying process, the more likely the process is to winiii.

THE 90%

Every active manager has seen the comparison below that 90% of active managers underperform their benchmark (Table 2). It’s depressing.

Here’s the positive. There is a way to increase the chance that you are not part of the 90%.

Our data (Table 1) suggests that fundamental research and stock picking are not the problem. The Alpha Theory Optimal return is a measure of fundamental research and stock picking skill because the optimal sizes are calculated using the price target forecasts and conviction levels scored by the analysts. The research-based sizing (Optimal) outperforms AT Client Performance by 4.3% (11.5% vs 7.2%, respectively).

An equal-weighted portfolio, which is pure stock selection and includes no sizing skill, outperforms active managers’ sizing by 1.6%. Active position sizing reduces returns!

The good news. The data confirms there is research skill. And there is an easy way to get even better returns from this alpha-rich research as the Alpha Theory version of the portfolio outperformed equal-weight by 2.7%.

PROCESS ENHANCES PERFORMANCE

Alpha Theory clients are a self-selecting cohort who believe in process and discipline. Below are some of the best lessons for turning process into performance.

START WITH PRICE TARGETS

Alpha Theory research shows that positions with price targets outperform those without price targets.

The ROIC for long equities with price targets is 4.9% higher than those without price targets. The outperformance is even greater on the short side, where short positions with price targets outperform by 7.1%!

Some investors chafe at price targets because they smack of “false precision.” These investors miss the point because the key to price targets is not their absolute validity but their explicit nature, which allows for objective conversation of the assumptions that went into them.

In other words, the practice of calculating a price target and the questions that price targets foster are central to a good investment process.

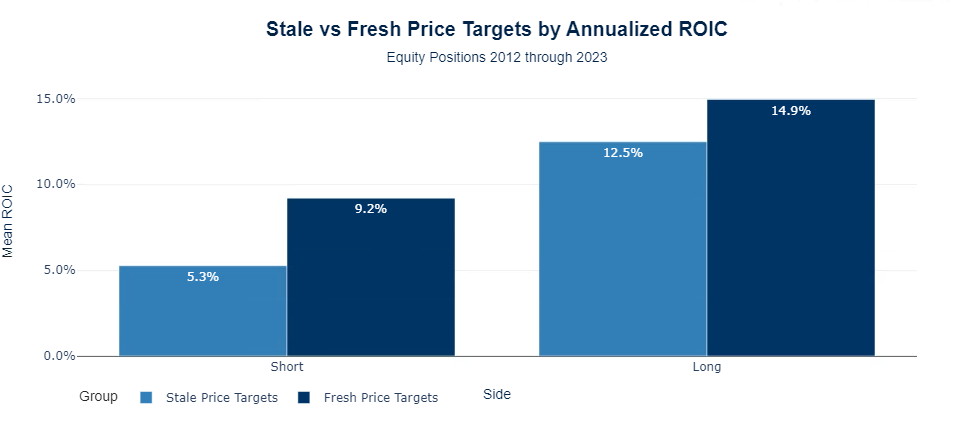

KEEP PRICE TARGETS FRESH

Once you establish price targets, keeping them fresh will further increase performance.

We observed a notable increase in ROIC for long and short equity positions, where fresh price targets were associated with an ROIC increase of 2.4% and 3.9%, respectively, compared to their stale counterparts (Figure 3).

ALIGN POSITION SIZE WITH IDEA QUALITY

The next step is to create a systematic process to highlight when positions are out of line with the research. That’s what Alpha Theory does in the form of optimal position sizing.

SYSTEMATIC POSITION SIZING OUTPERFORMS

Systematic position sizing (Optimal) outperforms actual position sizing in key metrics including ROIC, batting, slugging, and returns from the average winner (Table 3).

These findings, observed over twelve years and 100+ managers, give us confidence in the value investors can realize by more closely following the system they built in Alpha Theory.

SYSTEMATIZE YOUR PROCESS

Become a part of the 10% of managers that outperform their benchmark. Let Alpha Theory help you systematize your process and discover alpha hidden in your portfolio. Book a demo here.