.svg)

Sometimes the Best Position Size Is 0%

Your smallest positions take focus and resources. But they also drag down alpha.

One common misconception we bump into with fundamental managers is that certain ideas deserve at least some capital so that it’s “on our radar” and will focus the teams’ efforts. It doesn’t. In fact, across hundreds of funds and nearly two decades of data, the evidence is consistent:

“Small positions drag down performance.”

Some investors call these positions “farm names.” Sound in theory, the idea is that “we’ll monitor it, see how it grows”. Managers might keep small, low-conviction names in the portfolio just as a means to keep them top of mind and quickly add them if anything changes. But this could be a costly practice. These sub-scale positions dilute exposure to your core ideas and create drag that compounds over time.

And the fix is often simple. Size them correctly. And many times, the correct size is zero. Let’s look at the data.

The Data: Small Positions Underperform

To measure the impact of smaller positions on portfolios, we analyzed hundreds of thousands of positions across hundreds of fundamental managers going back a decade. What we found was not a shock, but still fascinating to see. In short, the smallest positions are dragging on the rest of the portfolio for most managers.

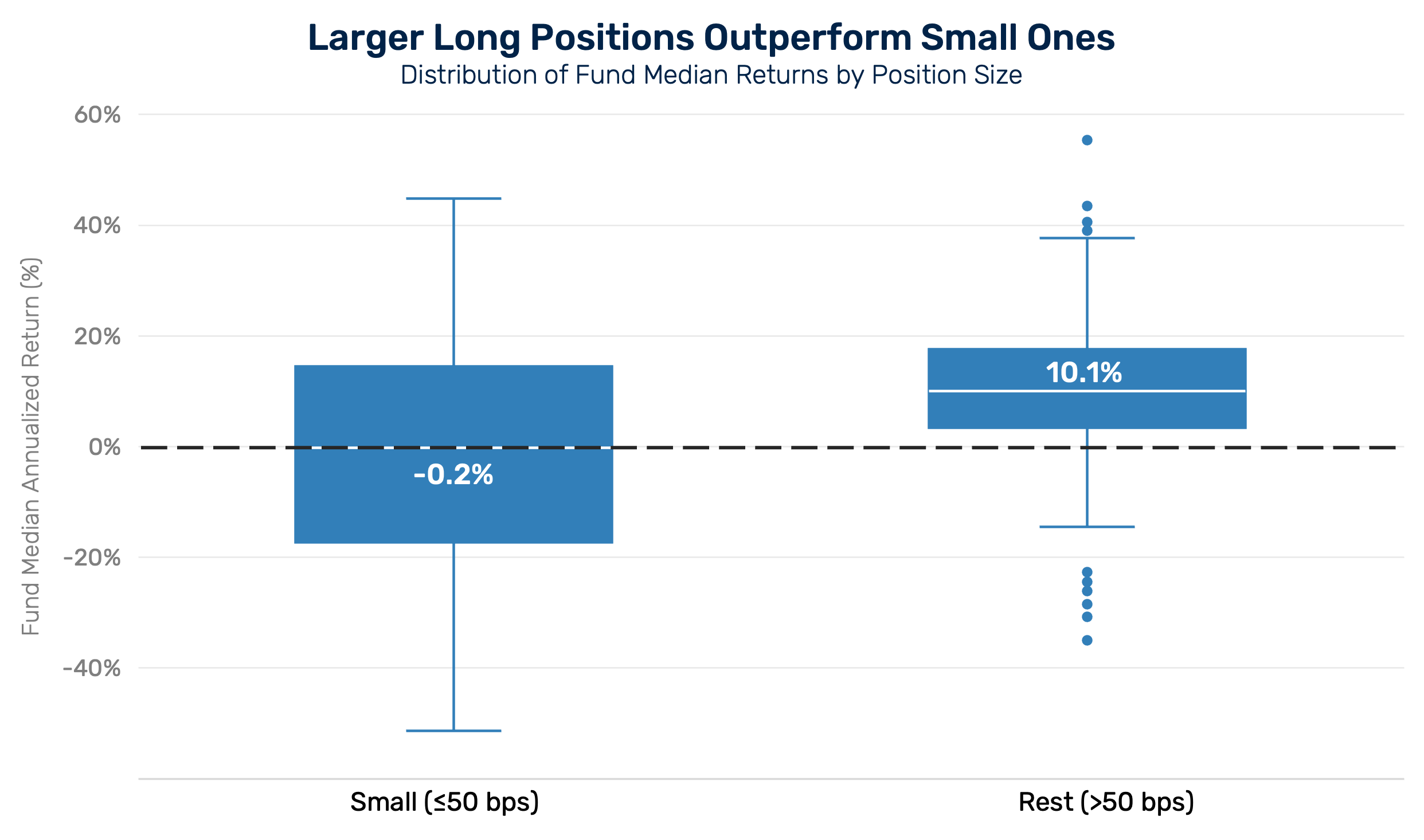

Bucketing long positions into two groups, under 50bps and the rest, we calculated the average returns for each, rolled them up to each fund, and then plotted the results. In this box plot, each fund gets two points – one in the small bucket and one in the “rest” bucket. Clearly, the averages show significant underperformance for funds on their smallest position sizes, and the average return on a small, long position is roughly flat (-0.20) for the average manager. Conversely, on the average name above 50 basis points managers are well in the green, registering an average return of 10% annualized for that segment. While both segments exhibit outliers, the smaller positions have a more negative skew. This means that not only do the smallest positions have lower returns on average, but the losers in the smallest position bucket (25th percentile) are worse than an average losing position overall.

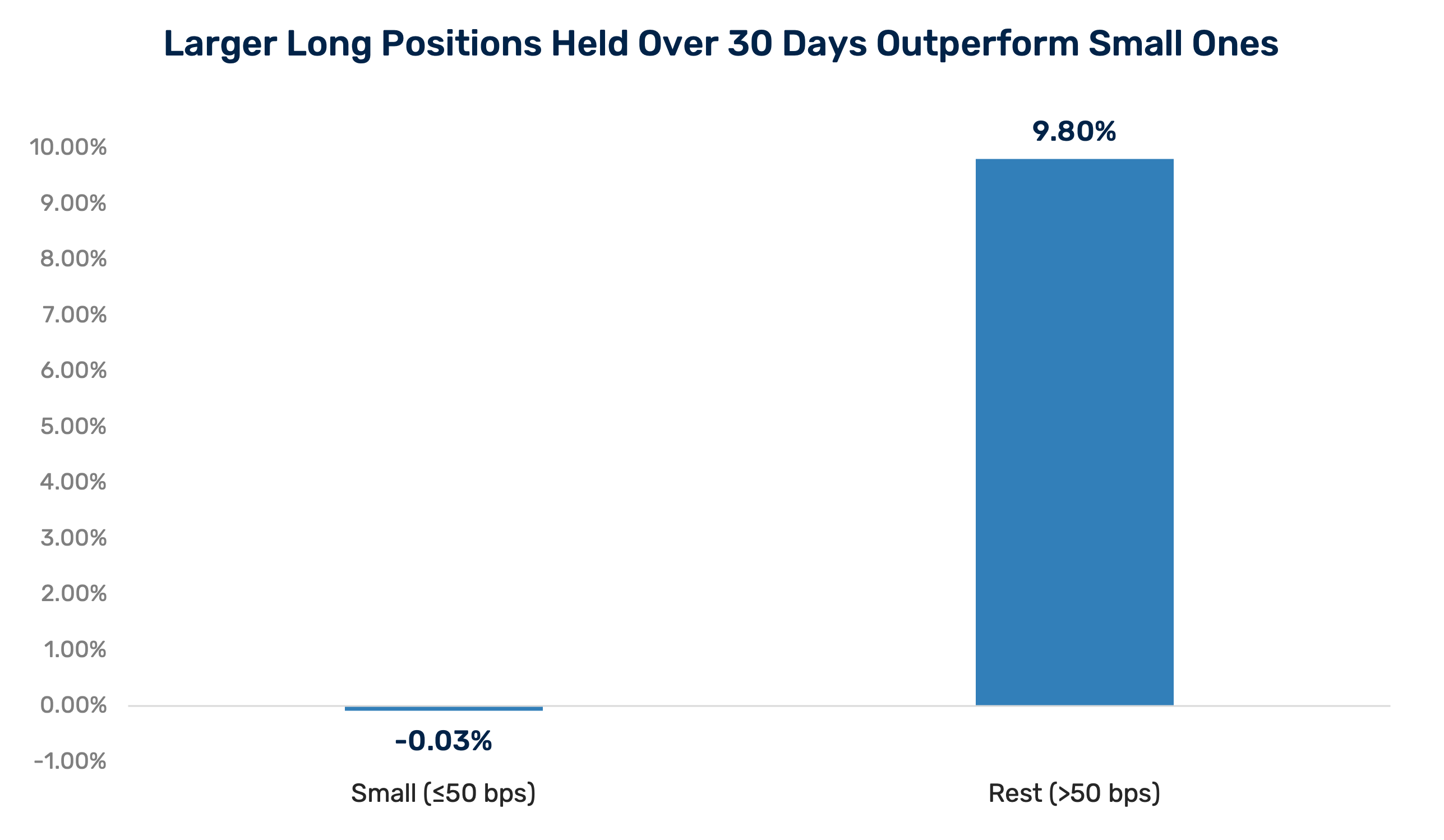

Looking at it through a slightly different lens, we focused on names that were held over 30 days and found the median returns for the two buckets across all managers. The smallest positions were again found to be a drag on performance, a whopping 10% below the other names.

We are not alone to find evidence of this. There are several other examples of research with similar findings.

As we noted in Ultimate Position Sizing Guide Part I, several analytics providers, also looking at thousands of positions across fundamental hedge funds found the same pattern:

- Largest positions generate the highest ROIC.

- Small positions systematically underperform.

Our friends at SEI Novus, for example, demonstrated that the smallest positions tend to deliver negative contributions relative to the rest of the book.

Multiple empirical studies (e.g., Clarke, deSilva & Thorley; Grinold; Wermers) show that while position sizing decisions explain a large share of the difference between good managers, the low-conviction, small positions contribute little alpha and often create uncompensated volatility across the board.

Why “Farm Names” Persist

Even elite managers can easily follow this line of thinking:

- Fear of missing out. “I have a good idea, I want to get it on before others figure it out and the stock moves.”

- Sunk cost bias. “We already did the work on it.” Since we invested the time, might as well invest some capital.

- Optionality thinking . A manager may reason “let’s keep it around just in case.”

- False idea of diversification. It’s important to note that farm names are not the same as satellite names that are more active and have a specific reason to be in a portfolio. Usually, satellite names go together in a theme with a core name; they either diversify exposure or amplify it. Farm names do not follow that pattern and tend to be less active.

We understand why managers may feel compelled to enter into a small position, but it pays to look at the data.

The Most Powerful Sizing Decision You Can Make

If you do not have conviction in a name to make it a meaningful size, data shows that there is no reason to have it at all.

Cut the left tail.

Eliminate positions that cannot justify meaningful capital allocation. In Alpha Theory, you can track them as “Ideas” and it can notify you of “Ideas” where a large position is suggested.

A zero percent position size is not a failure of research even if your team sunk days and weeks into it. Zero size just shows that you have sizing discipline.

If This Resonates, Go Deeper

We explain this concept in greater detail, and show empirical proof for the benefit of holding 10-30 positions for fundamental managers and stock pickers in our whitepaper: The Concentration Manifesto.

If you want the full playbook for improving sizing discipline, from identifying farm names, to building a repeatable sizing framework, the Ultimate Position Sizing Guide (UPSG) Parts I–III is a great resource.

- Part I: Why sizing matters (and how much alpha is left on the table)

- Part II: The mechanics, data, and proof behind structured sizing

- Part III: The seven steps to building an idea-aligned, repeatable sizing process

.png)