.svg)

The Missing Feedback Loop in Fundamental Research

Most fundamental managers already have excellent financial models. The trouble is that the model, the portfolio, and the record of how their forecasts actually turned out live in three separate places.

Introducing the Financial Model card and Excel Connect 1.3

Most fundamental managers already have excellent financial models. The trouble is that the model, the portfolio, and the record of how their forecasts actually turned out live in three separate places.

The pattern is familiar. An analyst builds a model, debates the assumptions with the PM, lands on a price target, and the team sizes the position. The quarter passes, actuals come in, consensus moves, and the model gets revised. The work keeps moving forward while the history of what the team believed, and how it compared to reality, scatters across old spreadsheets and memory.

That makes the questions worth asking hard to answer. Where were we different from the Street? Were we right to be? Which assumptions drove the price target? Which metrics did we forecast well, and where can we improve? And the one that matters most for sizing: should that track record change how much confidence we put behind the next forecast?

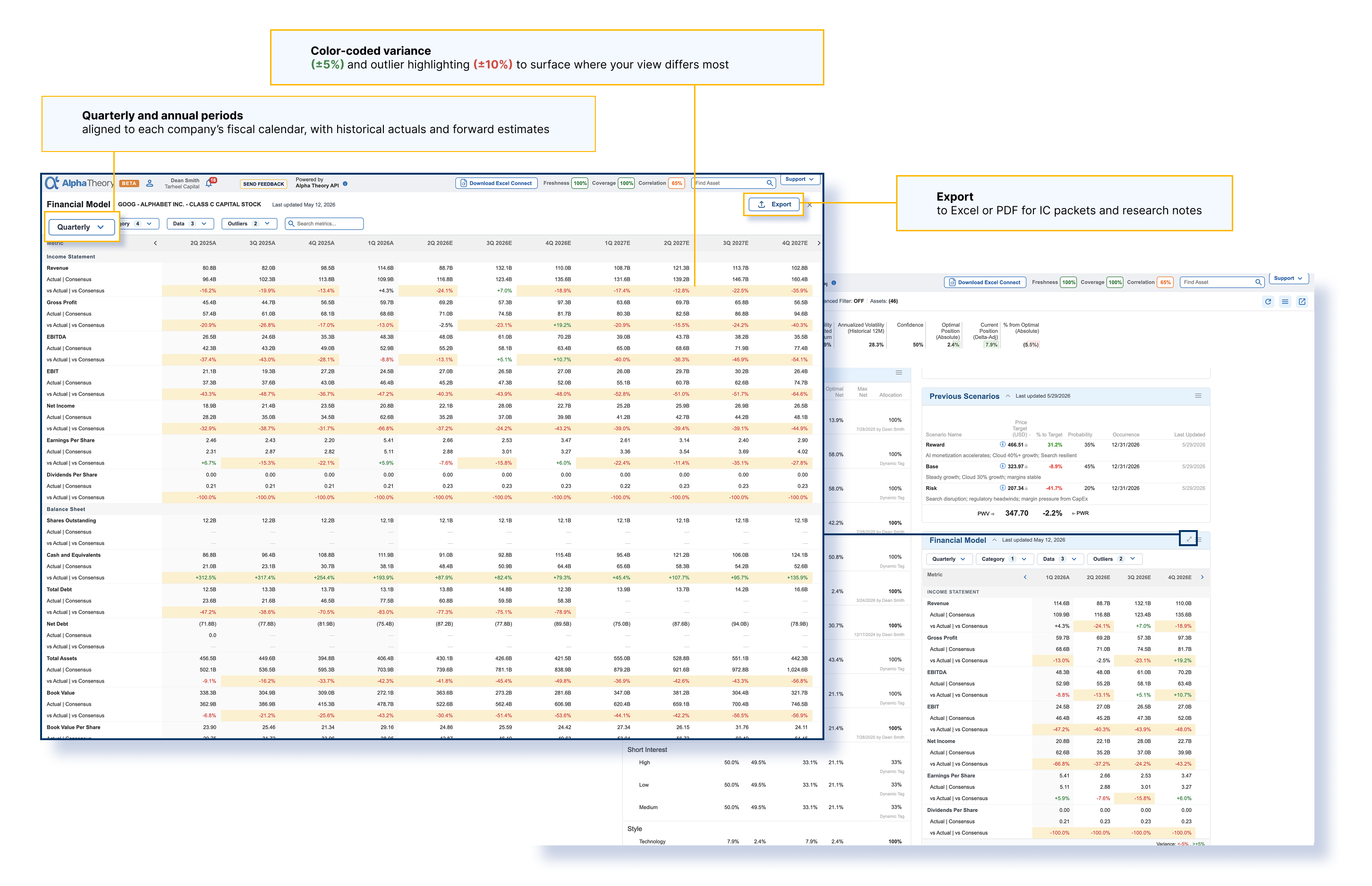

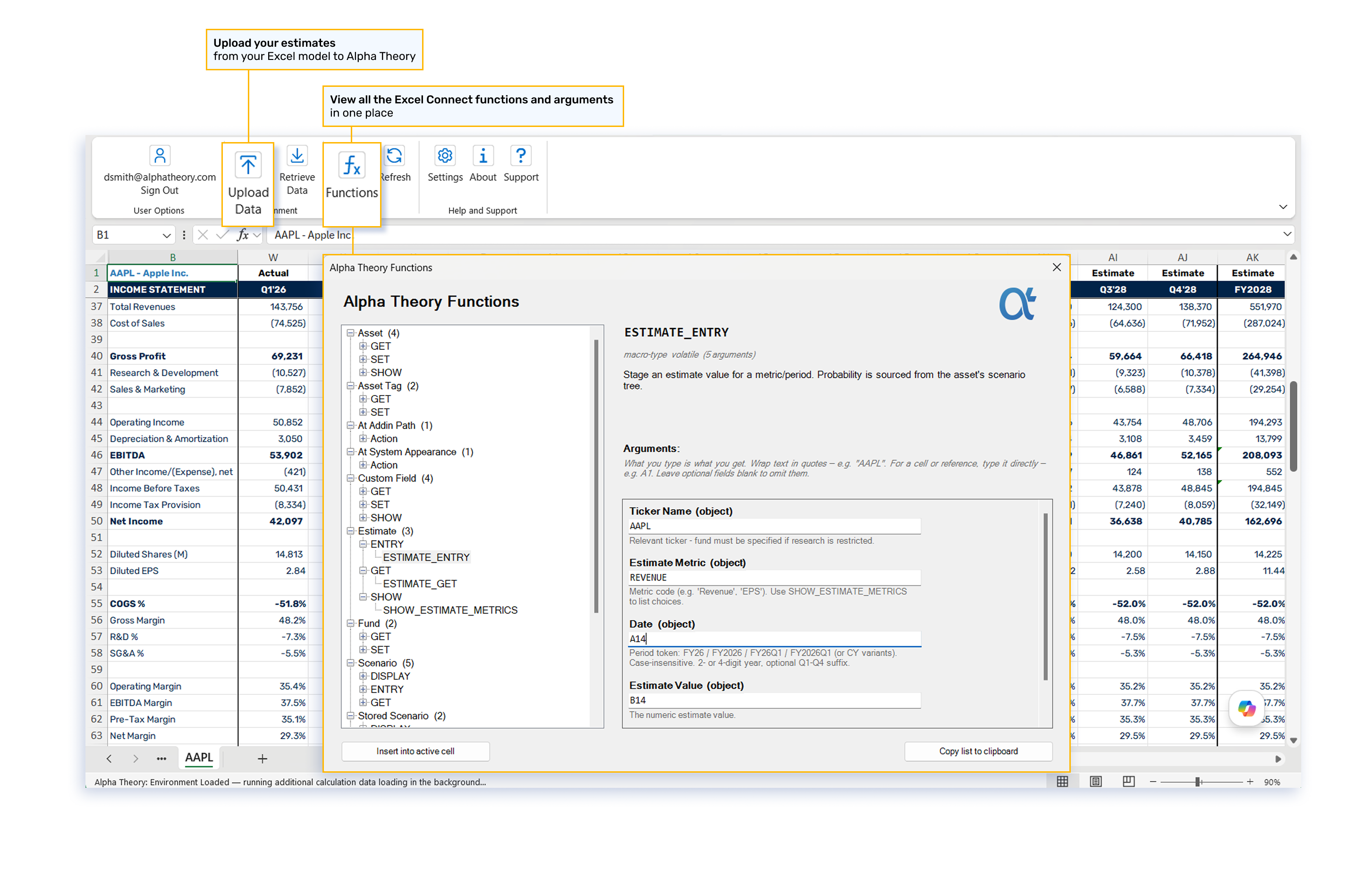

Financial Model card and Excel Connect 1.3 are built to answer those questions. Financial Model card brings your estimates and Street consensus into the same place where you already manage price targets, confidence, expected return, and optimal position size. Consensus and reported actuals are pulled in automatically through FactSet without any additional cost, and the variance against your numbers is calculated for you. Excel Connect 1.3 is the bridge: your Excel model stays the source of truth, with your estimates flowing into Alpha Theory.

For the analyst, this surfaces where the model is truly differentiated. A price target might rest on a broad view of the company, or the whole thesis might hang on one assumption about margins. Seeing your divergence next to the actual outcomes over time is how you measure real forecasting edge. For the PM, it is more direct. A PM might find an analyst has been excellent on gross profit and consistently too optimistic on EBITDA. Knowing that shows the PM exactly what to pressure-test before the view becomes a bigger position.

This is the discipline Alpha Theory has always been built around. Sizing improves when the link between expected return, confidence, and portfolio weight is explicit. Financial Model card and Excel Connect 1.3 push that one level deeper, into the assumptions that create the expected return in the first place.

Better research only turns into better sizing when the research has a feedback loop. This gives your team a clean record of what you believed, how it compared to the Street, what happened, and whether any of it should change your next move.

Take it for a spin and tell us what you think.